|

| www.gmsisuccess.in |

Blockchain, sometimes referred to as Distributed Ledger Technology (DLT), makes the history of any digital asset unalterable and transparent through the use of decentralization and cryptographic hashing.

“Blocks” on the blockchain are made up of digital pieces of information. Specifically, they have three parts:

- Blocks store information about transactions like the date, time, and dollar amount of your most recent purchase from Amazon. (NOTE: This Amazon example is for illustrative purchases; Amazon retail does not work on a blockchain principle as of this writing)

- Blocks store information about who is participating in transactions. A block for your splurge purchase from Amazon would record your name along with Amazon.com, Inc. (AMZN). Instead of using your actual name, your purchase is recorded without any identifying information using a unique “digital signature,” sort of like a username.

- Blocks store information that distinguishes them from other blocks. Much like you and I have names to distinguish us from one another, each block stores a unique code called a “hash” that allows us to tell it apart from every other block. Hashes are cryptographic codes created by special algorithms. Let’s say you made your splurge purchase on Amazon, but while it’s in transit, you decide you just can’t resist and need a second one. Even though the details of your new transaction would look nearly identical to your earlier purchase, we can still tell the blocks apart because of their unique codes.

- Digital assets are distributed instead of copied or transferred.

- The asset is decentralized, allowing full real-time access.

- A transparent ledger of changes preserves integrity of the document, which creates trust in the asset.

How Does Blockchain Work?

The whole point of using a blockchain is to let people — in particular, people who don't trust one another — share valuable data in a secure, tamperproof way.

Blockchain consists of three important concepts: blocks, nodes and miners.

How Blockchain Works

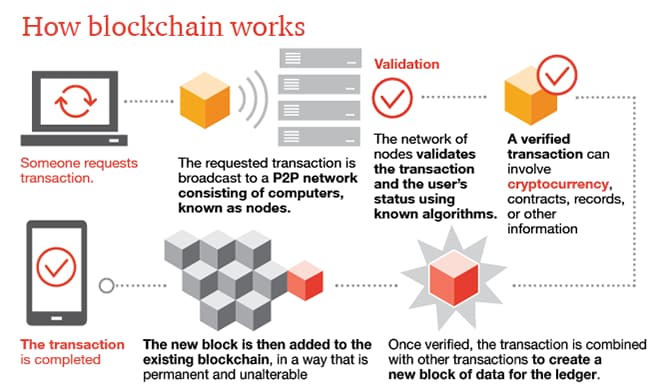

When a block stores new data it is added to the blockchain. Blockchain, as its name suggests, consists of multiple blocks strung together. In order for a block to be added to the blockchain, however, four things must happen:

- 1. A transaction must occur. Let’s continue with the example of your impulsive Amazon purchase. After hastily clicking through multiple checkout prompt, you go against your better judgment and make a purchase. As we discussed above, in many cases a block will group together potentially thousands of transactions, so your Amazon purchase will be packaged in the block along with other users' transaction information as well.

- 2. That transaction must be verified. After making that purchase, your transaction must be verified. With other public records of information, like the Securities Exchange Commission, Wikipedia, or your local library, there’s someone in charge of vetting new data entries. With blockchain, however, that job is left up to a network of computers. When you make your purchase from Amazon, that network of computers rushes to check that your transaction happened in the way you said it did. That is, they confirm the details of the purchase, including the transaction’s time, dollar amount, and participants. (More on how this happens in a second.)

- 3. That transaction must be stored in a block. After your transaction has been verified as accurate, it gets the green light. The transaction’s dollar amount, your digital signature, and Amazon’s digital signature are all stored in a block. There, the transaction will likely join hundreds, or thousands, of others like it.

- 4. That block must be given a hash. Not unlike an angel earning its wings, once all of a block’s transactions have been verified, it must be given a unique, identifying code called a hash. The block is also given the hash of the most recent block added to the blockchain. Once hashed, the block can be added to the blockchain.

When a block stores new data it is added to the blockchain. Blockchain, as its name suggests, consists of multiple blocks strung together. In order for a block to be added to the blockchain, however, four things must happen:

- 1. A transaction must occur. Let’s continue with the example of your impulsive Amazon purchase. After hastily clicking through multiple checkout prompt, you go against your better judgment and make a purchase. As we discussed above, in many cases a block will group together potentially thousands of transactions, so your Amazon purchase will be packaged in the block along with other users' transaction information as well.

- 2. That transaction must be verified. After making that purchase, your transaction must be verified. With other public records of information, like the Securities Exchange Commission, Wikipedia, or your local library, there’s someone in charge of vetting new data entries. With blockchain, however, that job is left up to a network of computers. When you make your purchase from Amazon, that network of computers rushes to check that your transaction happened in the way you said it did. That is, they confirm the details of the purchase, including the transaction’s time, dollar amount, and participants. (More on how this happens in a second.)

- 3. That transaction must be stored in a block. After your transaction has been verified as accurate, it gets the green light. The transaction’s dollar amount, your digital signature, and Amazon’s digital signature are all stored in a block. There, the transaction will likely join hundreds, or thousands, of others like it.

- 4. That block must be given a hash. Not unlike an angel earning its wings, once all of a block’s transactions have been verified, it must be given a unique, identifying code called a hash. The block is also given the hash of the most recent block added to the blockchain. Once hashed, the block can be added to the blockchain.

Blockchain vs. Bitcoin

The goal of blockchain is to allow digital information to be recorded and distributed, but not edited. That concept can be difficult to wrap our heads around without seeing the technology in action, so let’s take a look at how the earliest application of blockchain technology actually works.

Blockchain technology was first outlined in 1991 by Stuart Haber and W. Scott Stornetta, two researchers who wanted to implement a system where document timestamps could not be tampered with. But it wasn’t until almost two decades later, with the launch of Bitcoin in January 2009, that blockchain had its first real-world application.

The Bitcoin protocol is built on the blockchain. In a research paper introducing the digital currency, Bitcoin’s pseudonymous creator Satoshi Nakamoto referred to it as “a new electronic cash system that’s fully peer-to-peer, with no trusted third party.”

The goal of blockchain is to allow digital information to be recorded and distributed, but not edited. That concept can be difficult to wrap our heads around without seeing the technology in action, so let’s take a look at how the earliest application of blockchain technology actually works.

Blockchain technology was first outlined in 1991 by Stuart Haber and W. Scott Stornetta, two researchers who wanted to implement a system where document timestamps could not be tampered with. But it wasn’t until almost two decades later, with the launch of Bitcoin in January 2009, that blockchain had its first real-world application.

The Bitcoin protocol is built on the blockchain. In a research paper introducing the digital currency, Bitcoin’s pseudonymous creator Satoshi Nakamoto referred to it as “a new electronic cash system that’s fully peer-to-peer, with no trusted third party.”

KEY TAKEAWAYS

- Blockchain technology underlies cryptocurrency networks, and it may also be used in a wide variety of other applications as well.

- Blockchain networks combine private key technology, distributed networks and shared ledgers.

- Confirming and validating transactions is a crucial function of the blockchain for a cryptocurrency.

- Blockchain technology underlies cryptocurrency networks, and it may also be used in a wide variety of other applications as well.

- Blockchain networks combine private key technology, distributed networks and shared ledgers.

- Confirming and validating transactions is a crucial function of the blockchain for a cryptocurrency.

No comments:

Post a Comment